Let’s be real. Collection of student loan payments has been a complete roller coaster since the beginning of the pandemic, when they were paused by the Trump Administration. The Biden Administration then extended those pauses, introduced new payment options in order to lessen the burden on borrower’s, and then proceeded to soften the on-ramp back into repayment-time.

This new Trump Administration is ready to collect. And they are coming in hard.

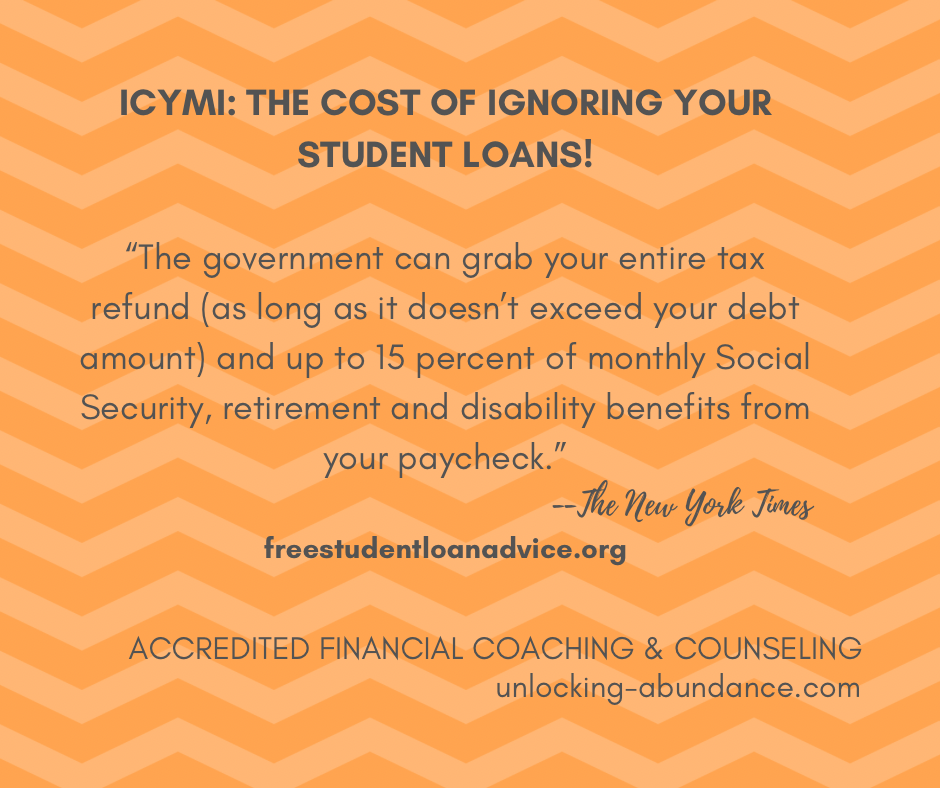

If you are currently in “default” on your student loans (defined by loans overdue by 270 days or more) which is currently affecting ALOT of borrower’s (more than 5 million!) you could soon be affected by wage garnish.

Your Next Steps as a Borrower: Log into studentaid.gov and gain an understanding of your loan(s) and balance due. You can also see if you’re on the right payment plan for you, or eligible for any forgiveness programs. As of this writing, SAVE, a Biden Administration program aimed at making student loan payments more affordable, is still held up within court battles, with no payment due.

Your Next Steps as a Borrower in Default: Check your balance situation. Give yourself grace. There are MANY borrower’s in your shoes right now. This summer, you may receive a notification by email of wage garnish notification. The email will contain a link for Debt Resolution with Federal Student Aid. Connecting with this department is your first step towards getting back on track.

You want to get your Student Loan issues resolved, and here’s why. Like many other types of borrowing, missing a Student Loan payment does impact your credit score. Current data shows that credit scores of millions of borrower’s are already plunging as the reprieves of non-payment are being lifted.

Why is this important? A dip in your credit score affects your ability to borrow at a preferred rate. If you have any existing issues managing debt, this only pushes you deeper into the pit of borrowing, as you’re being charged a premium on purchases simply due to your credit score range.

Unlike other types of debt, Student Loans will follow you essentially forever, they are usually not dischargeable even through bankruptcy, with some possible exceptions. Student loan debt is treated like the following types at the most serious level: child support, criminal penalties, federal tax bills, etc. Do your best to prioritize this debt and find a payment amount that works for you. I promise you–there is a better way to manage.

How should you prioritize your other types of debt? When it comes to the more “familiar” debt, such as consumer debt (credit cards), mortgages, auto loans, and other types of personal or housing loans, first look at the length of the term of the loan. If you have a comfortable payment amount, and you know you have a set time-frame to pay it off, you may not need to prioritize this debt. Next, look at the Interest Rate on the loan. If it is below 7%, you likely do not need to prioritize this debt. Make your payments on time. Rinse, repeat.

Identify your highest interest rate debt. This debt is common with credit cards, as the typical APR in the US right now is 20%+. That means you will pay an extra 20%+ annually on any amount that you continue to roll over. That $3000 couch? You may pay up to $600 in interest, just because you let that balance roll over. Depending on your purchase price, this can quickly become very expensive!

Ready to approach your credit card debt? You can do this. Again, get clarity on your balances and their interest rates. Whether you like the idea of the psychological hit of paying off a balance right away, or knowing that your plan might take longer, but saves you money over the long-run, there’s a strategy for that. Finally, who doesn’t love a good credit-card debt pay-off hack?

What would it feel like to not only believe you have a handle on your debt, but start to see the evidence in the numbers?