A quick update on student loan forgiveness, containing especially crucial news for borrowers who are enrolled in “SAVE”, the income driven repayment plan! Essentially, this particular plan has been blocked by the courts and there are no payments due at this time, nor will any interest accrue while the administrative stay is in place.

Read below for more information on what happened and, most importantly, what you can do in the meantime to set yourself up for success!

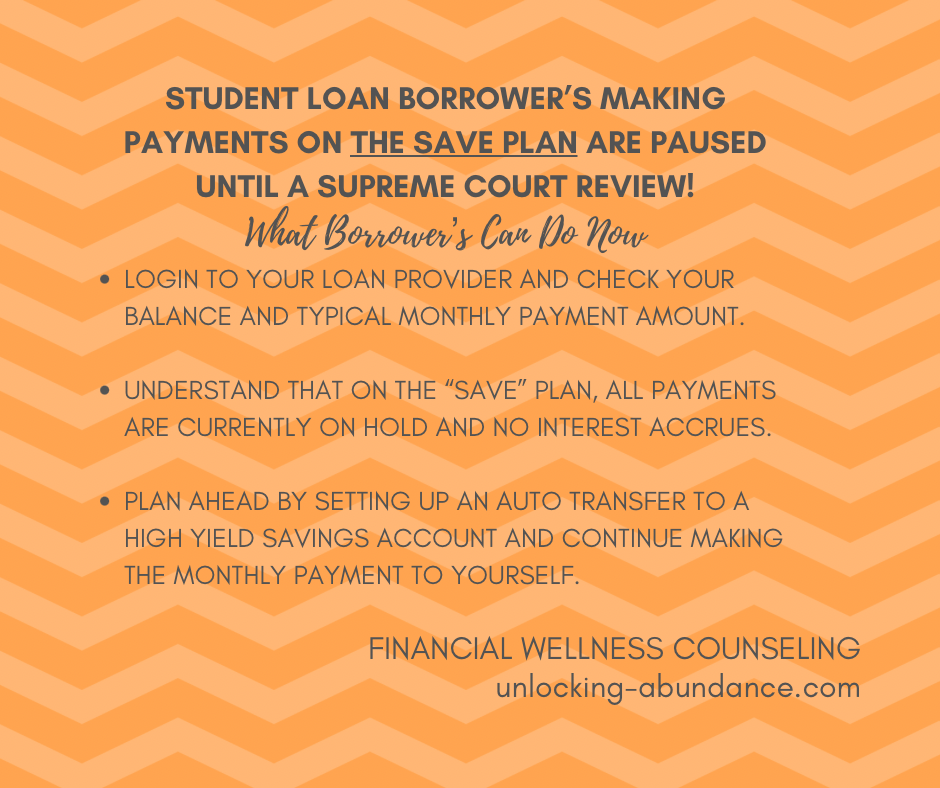

What Happened with SAVE?

ICYMI, on Friday, the 8th Circuit Court of Appeals completely blocked the Saving for a Valuable Education (SAVE) student loan repayment plan from moving forward, solidifying what had already been a temporary partial blockage back in June. An “Administrative Stay” was granted stating that borrowers already on the plan are now, temporarily, considered to be in “forbearance”. (Forbearance is typically an option used to pause payments for borrowers that is determined by the lender, versus a “deferment” whereas the borrower makes the request and has to get it approved.)

What is SAVE and Why is this so Impactful?

SAVE, introduced in 2023, was introduced by the Biden Administration as a sweeping overhaul to income-driven-repayment (or IDR) payment plan options. The biggest draw is that SAVE restructures the amount of money borrowers are required to pay towards their student loan debt by taking into greater consideration their amount of discretionary income (money leftover after paying their “Needs”). Many borrowers had no payment due on SAVE. The plan also included a provision against interest accruing faster than balances could be paid off. Currently, SAVE has enrolled 8M borrowers!

What Can Borrowers Do Next?

If you wanted to get on the SAVE plan, and hadn’t applied yet, no applications are being taken during this time. There is no indication of when we might be instructed on what will happen next.

If you’re a borrower enrolled in SAVE..a good strategy is to ‘hope for the best, plan for the worst’. In other words, identify what is within your control right now. Can you login and reacquaint yourself with your student loan balance and usual payment amount? Can you repurpose the amount you were paying towards your loans, to be inline with a financial goal?

You might look at a recent bank statement to see what you had been paying before the pause. If you had a manageable payment amount, this is your opportunity to enact a “pay yourself first” plan! This could look like identifying your payment amount and due date, and setting up an auto-transfer to your own savings account (High Yield Savings Account being the first choice because of their accessibility, high interest, and virtually no-risk). You have the opportunity, right now, to grow that money you were sending towards your student loans, for yourself!

As time goes by, which of course it’s going to anyway, you’ll be stockpiling your own student loan payments, and you can pull from that account if/when the payments do start up again (very likely) and if you never have to use that money for student loans, it’s your money to use however you choose! Alternatively, if you have any high interest debt (usually counted as being debt at higher than 7% interest–think credit card debt) you could take the student loan payment you were making, and pivot it towards the debt!

Again, there is currently no guidance around when this stay on payments will be resolved, but you do have full control over what you can do with money you were using to make those payments!

What could you do, right now, that would have the biggest impact on your financial goals? How good would it feel to move towards that direction?