Last week we went over your Tax Filing Checklist in order to get organized for filing this year, but some people might also want to know..how can I lower my taxes?

Read below for a few, and perhaps, lesser-known ways to lower your tax liability! As always, not tax advice—just some friendly financial literacy!

If you find filing your taxes to be uber-confusing, you are not alone. It’s almost as if the system is set up in order to burden you with the task of paying someone to figure it all out for you, right? Luckily, we do have some free file options!

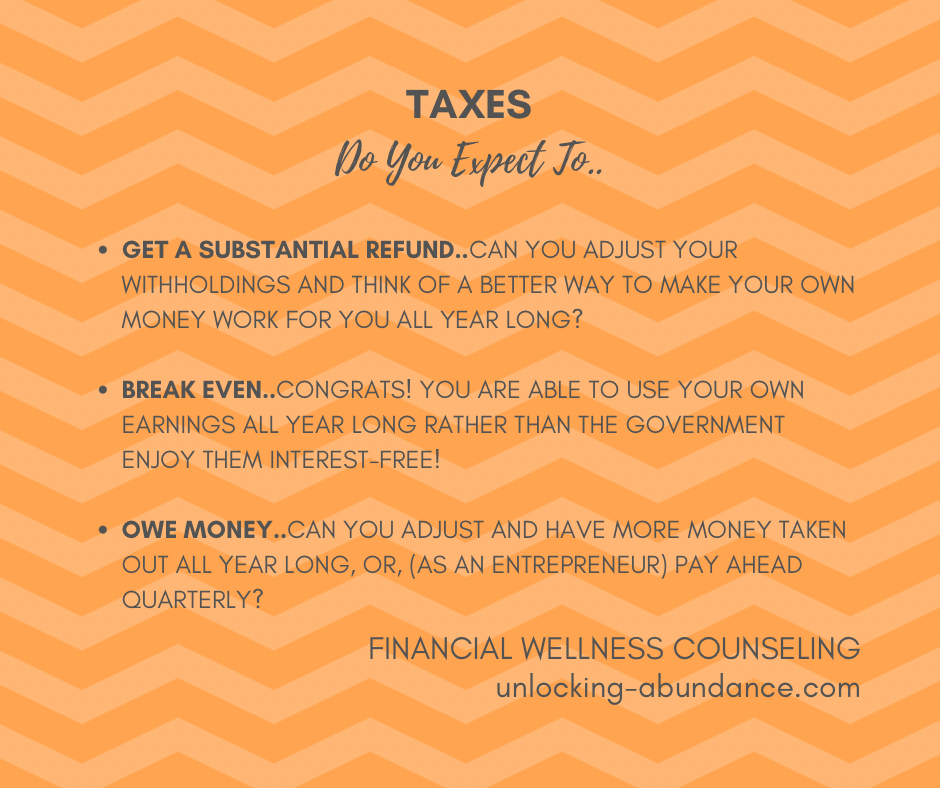

Starting with the basics, this season, when thinking about filing your taxes..do you expect to:

Get a Refund..if so, you overpaid, tax-wise, all year long and the balance is refunded to you. How might you make the most of this money by keeping it for yourself during the year, rather than letting the government hold onto it? You could put it into a High Yield Savings Account? Invest? Your money could work for you, rather than for the government.

Break Even..if so, you paid just the right amount for your tax liability! You cracked the system! You were able to keep and use your own money all year.

Owe..if so, you didn’t pay enough all year long and now the bill is due. You may want to look into adjusting the amount being pulled from your paycheck. Or, as an entrepreneur or someone working without taxes being taken out for you, you might be required to pay Estimated Quarterly Taxes (see more on this below) which can lessen the impact at tax time.

A Few Ways You Might Lower Your Tax Liability This Year:

–Adjustments on the Income Side.

–Be Eligible for More Deductions. (Especially important for self-employed folk.)

–Be Eligible for More Credits.

–Contribute to a tax-deductible Savings Account like a Retirement Savings Plan/401(k) or a Medical Savings Account.

On the Income Side:

You might be able to lower your tax liability if you increase the amount your employer takes out. This would require you to request a copy of your W-4 that your employer has on file. The more “withholding allowances” you have on file, the more you are keeping your own money and thus may have a larger tax bill. Conversely, if you claim “zero allowances” you are telling the employer that you want the maximum withheld and you might have more chance of overpaying the government and getting a refund.

Based on the amount you owed in taxes last year, take the amount you think you might owe this year and see on your paystub what is actually being pulled from your check for Federal Taxes. If it doesn’t look like the amount they’re taking out will cover you, you can then break it down into a monthly cost and request that your employer take that amount out, per month, or inline with however often you are paid.

Self-Employed or Contract Workers who do not have taxes withheld for them, may be required to pay their tax liability in advance, making Estimated Quarterly Tax Payments to the IRS. The general rule is that if you consistently owe more than $1k at tax time, you may be required to pay in advance. Penalties may be assessed for missed payments.

Deductions:

Deductions lower your income, therefore lowering your tax owed. You might contribute to a tax-deductible account like a Traditional IRA or 401(k) Retirement Savings Plan, or Health Savings Account like an FSA or HSA. Making these payments directly lowers your taxable income by the amount of the contribution. For example, if you made $50,000 and contributed $5,000 to a tax-deductible 401(k), you would only pay tax on $45,000. (See even more tax advantages of contributing to a Retirement Savings Plan in the “Saver’s Credit” below!)

For Entrepreneurs and Contract Workers (tip: consider using a certified tax preparer in order to maximize all business deductions) business “write-off’s” lower your taxable income by tabulating what it cost you to do business. Find a list of eligible business deductions here.

Credits:

Some tax credits lessen the amount of tax you owe, and some put money directly back into your pocket if they are greater than what you owe.

Child and Dependent Care Credit is available for those who have to pay for childcare in order to work. Eligibility is based on income limits. You will need to provide the legal Tax ID Number for the organization paid, or the SS# of the individual doing the care. Check your eligibility!

Lifetime Learning Credit is available for those with tuition or educational expenses such as continuing ed or any class, or classes, that relate to job-training and/or improving your working skills. The credit is for tuition/fees/books, or anything required for that specific course. Even taking a single course applies, as long as it’s at an accredited institution. Income limits apply. See if your institution qualifies!

Retirement Savings Contribution Credit or “Saver’s Credit” is available for those in certain income brackets making retirement contributions. Eligibility is based on filing status and how much you contributed.

Energy & Environmental Credits may be available for Electric Vehicles purchased in 2023. Home upgrades such as heating/cooling systems also have rebates. Check your own eligibility.

The Working Families Tax Credit, new in the last 2 years, is a cash refund on Washington State Taxes, that applies to working families in WA State who meet the income limits. The refund amount is adjusted depending on family size. You must have been a WA State resident for at least ½ the year for the tax year you’re filing. See if you qualify! (Tip: for this one, you need to have filed your federal taxes first and then you may be eligible.)

However you do your taxes, take the time to read through and research what may or may not apply to you–you may be eligible for more than you think, thus keeping more of your own hard-earned money! How good would that feel?