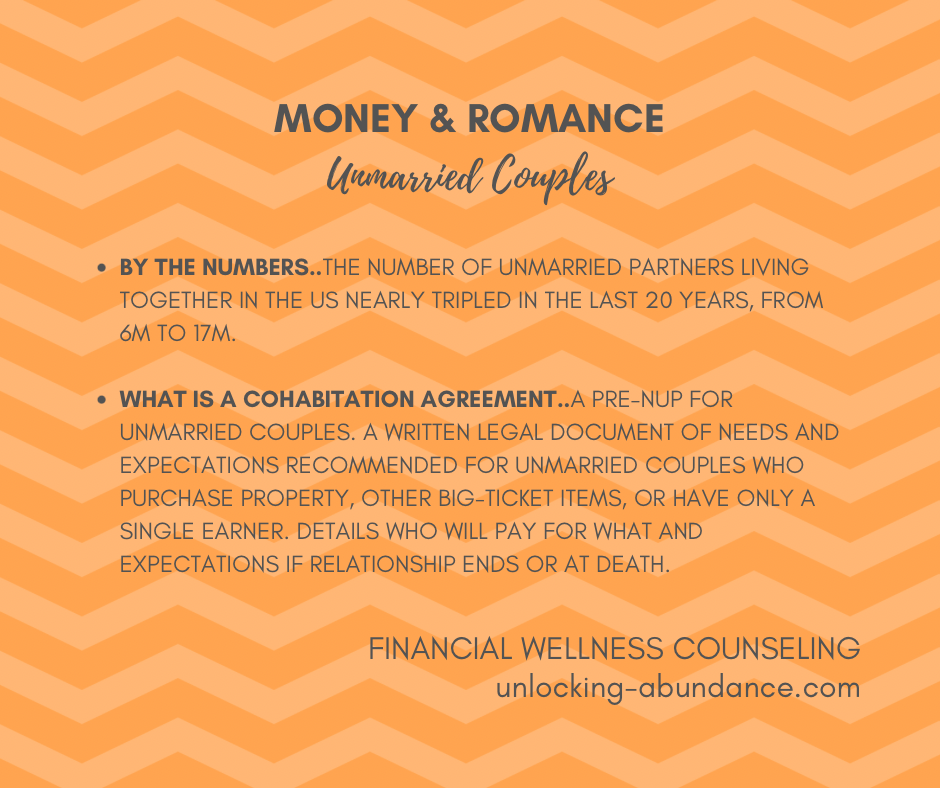

Continuing down the love & money path..odds are, you or someone you know is living together in a partnership unmarried. This is a growing group of people! At the end of 2022, for example, 17M people were living together but not married. That’s three times as many as twenty years prior! 15% of people aged 25-34 live together unmarried. That’s up versus 10 years ago, and the amount of 65+ aged people cohabitating has increased threefold since nearly twenty years ago.

Why are Not as Many People Getting married?

Along with a general shift in traditional family values, many younger people today are the product of divorce themselves and perhaps don’t want to go through that experience. The divorce process can be not only highly stressful, but very expensive.

When it comes to finances, unmarried couples may value maintaining their own autonomy and control over their own assets. Some may see value in the freedom of avoiding joint tax-filing implications and restrictive state-by-state laws around shared property.

What are the Options for Splitting the Expenses?

There is no right or wrong way here, it’s whatever works best for your household. When it comes to splitting the shared expenses, one option is to simply divvy up the shared bills either equally (or in line with income equitable to what each person earns). Both people agree to what they will be responsible for, and take care of it from their own bank accounts.

If you do decide to dabble in combining finances, you can do this partially without diving all in. You could open a joint checking account that will be used only to pay the bills that you’ve identified as shared. Ideally, all of these bills should be set up on auto-pay from this account and transfers should be on auto-pay to fund the account. This method takes a little time to set up, and requires a lot of trust to ensure that everyone will hold up on their end.

Leveling up could look like opening one more joint account, a HYSA savings account, that you can both funnel money into, again automatically, for shared goals and emergencies.

Caution: understand that joint accounts can be drawn down to zero by any signer on the account, at any time, no questions asked. Trust and transparency are essential when sharing anything financial; just having a joint account has been shown to build trust in the relationship.

Who Needs a Cohabitation Agreement?

Cohabitation Agreements are essentially prenups for unmarried people. They’re legally drafted contracts that detail what to expect, financially, for the partnership. They can chart a plan for what the financial responsibilities and expectations will be in the relationship: beginning, middle and end (if it should be so).

They can detail the name(s) on titles of property and big-ticket items, as well as how bills will be shared. They can include how things will be split if the relationship were to dissolve and deadlines for having everything finalized.

Since there is no method to resolve property rights for unmarried people and no legal ground to claim rights to another’s income, like there would be in a divorce, these types of agreements can be attractive for couples in specific situations we may not think about. For example, if one person works and the other does not (takes care of the children perhaps) that non-working partner could get stuck with nothing, or a less than desirable outcome, if agreements are not decided on in the beginning.

Can you think of a financial situation you’re in right now with another person that could get messy? What would be the pro’s and con’s of putting something formal in place?