Let’s talk Health Insurance Benefits!

It’s nearly that time of year where we sit down and decide our health coverage for next year, otherwise known as Open Enrollment.

If you’re lucky enough to have health insurance benefits through your employer, during Open Enrollment, you may be presented with a variety of plans that your company offers. If you’re self-employed or don’t have health insurance through work, the burden may be on you to decide your coverage. Either way, you may see the terms Flex Spending Account (FSA) or Health Savings Account (HSA) thrown around. If you’re anything like the average human, you have no idea what these mean and how to weigh them against each other. Well, these are actually health insurance benefit add-ons and each have their pro’s and con’s.

Read below for what a FSA is, what a HSA is, and which might be right for you.

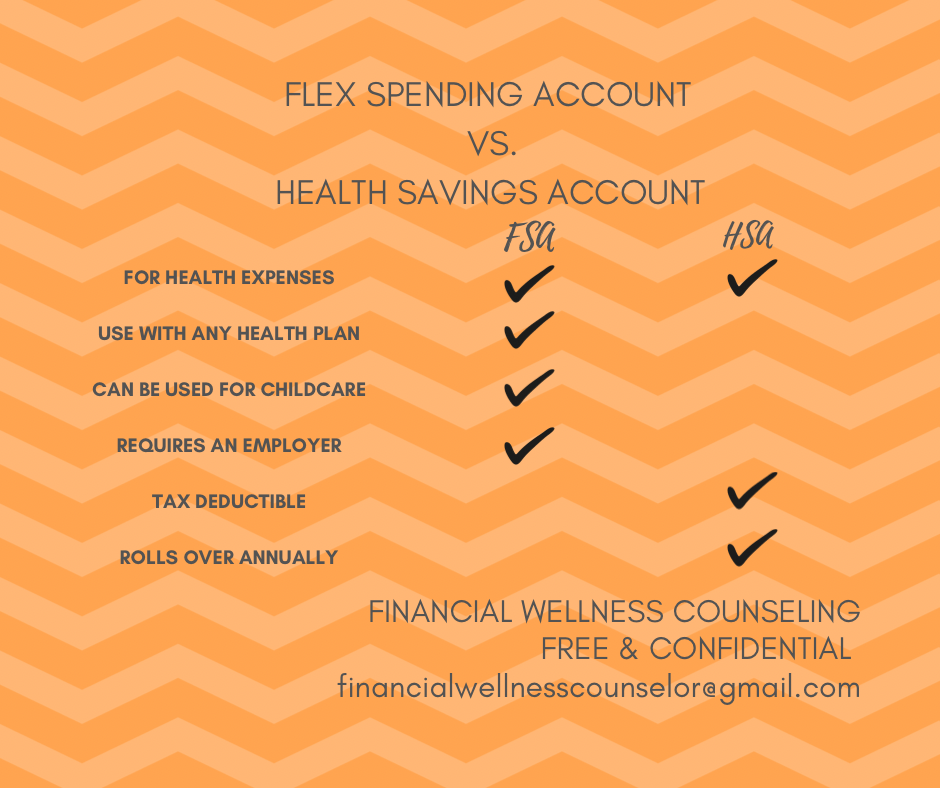

Similarities: Both a FSA and HSA are used to help you set aside funds for medical expenses in a tax-advantaged way, without using your hard-earned cash that you’ve already paid tax on.

If you have either of these through an employer, employers can also make contributions to these accounts; if this is the case, yay–free money! Money goes into the account tax-free, and you also won’t pay tax when you spend the money in your account on qualified medical expenses. The math works out that you are using tax-free dollars to pay for medical costs, thus saving up to 30% on that bill!

FSAs and HSAs are each subject to an annual contribution limit: currently $2850/Single and $3650/Single/$7300/Family (HSA includes Family) in 2022, respectively. Both accounts let people aged 55 and older make an additional catch-up contribution of $1,000 per year.You may not have an FSA or HSA if on Medicare.

FSA Pro’s: A big advantage of FSA is that all your funds are available immediately the day you enroll. In other words, your employer fronts you the money and then as you use it is deducted (tax-free) from your paycheck until it is repaid. You can also use FSA with any health insurance plan.

FSA Cons: FSA’s are provided by your employer (these are not available to the self-employed). This means your employer — not you — owns your FSA account. If you leave your job, you lose your FSA funds. The biggest drawback to an FSA is that the money in the account is “use it or lose it,” meaning you lose whatever money you don’t use up by the end of the year.

FSA Extra Tip: FSA is the only of these two vehicles to be able to be used for childcare. You can have a Dependent Care FSA at the same time as having a HSA. A Dependent Care FSA is a separate account you can sign up for at work, if your employer offers it. These accounts are used to pay for “eligible dependent care services” including preschool, summer day camp, after-school programs, etc. In 2022, you can contribute up to $5,000 per year to a Dependent Care FSA.

HSA Pro’s: You hold your own HSA; it doesn’t have to be through an employer–especially great for entrepreneurs! You can use the money any time for medical expenses, and you’ll never pay taxes on it. The account rolls over year after year, you do not have to use it by the end of the year. If you withdraw money for non-medical expenses before age 65, you’ll owe the IRS a 20% penalty, plus have to claim it as income. After age 65, you can withdraw money from an HSA penalty-free for any reason, although you’ll still pay income tax. In that way, it works a lot like a 401(k). This is another way to grow money for retirement tax-free! You can even keep your receipts and reimburse yourself retroactively years later! If you contribute to a HSA outside of an employer with already taxed money, you can write it off on your tax return each year.

HSA Con’s: You must be enrolled in a “high deductible” health insurance plan to qualify, which means premiums may be higher. In 2022, the minimum deductible to qualify for a HSA is at least $1,400 for self and $2,800 for family.

Not sure where to start?

Ask yourself these questions: Am I self-employed or am I an employee?

Does my employer offer an FSA or HSA account?

How expensive do I think my medical bills will be next year?

Will my deductible qualify me for a HSA?

Do I want the account to be portable so I can access the money when I change jobs?